Auto Loan

Classic Car Loans in 2023

Unhappy with your current auto loan terms? Click here to refinance and drive home some savings!

Unhappy with your current auto loan terms? Click here to refinance and drive home some savings!

Key Takeaways

When someone says "classic cars," it's unclear what they mean. What constitutes a "classic "car is a matter of opinion and definition. Generally, a classic car is at least 25 years old, though this age range is flexible. The Classic Car Club of America defines classic cars as "Fine" or "Distinctive" automobiles manufactured between 1915 and 1948.

Classic cars can cost a lot of money. But, in addition to being a safe investment, their value tends to rise over time, setting them apart from most automobiles. So, if you can get approved for a classic car loan, you can purchase your dream classic car. It may be challenging to secure financing for a classic car, but it is not impossible.

Your first stop should be at your local bank or credit union, the institution that issued your mortgage, or the company that has provided financing for your usual mode of transportation. These are reliable jumping-off points. However, you may discover they have little familiarity with the classic and exotic car industry and have never written a loan to acquire a classic vehicle. So, to accomplish your need, you'll have to broaden your search.

The cost of a classic car is determined by several factors, including the model year, make condition, and rarity of the vehicle. If they're not in perfect shape, some of them could cost several thousand dollars. However, really rare and collectible versions might sell for millions.

Since many sales are conducted in secret, it is difficult to determine which vehicle sold for the highest price. As an illustration, a wealthy American entrepreneur reportedly spent $70 million on a Ferrari 250 GTO. The most trustworthy public record of classic car pricing can be found at auctions.

| Classic Car Lender | APR | Loan term | Amount |

|---|---|---|---|

| Woodside Credit | Rate Unavailable | Up to 180 months | $10,000- $1,000,000 |

| LightStream | 7.24%-15.19% | 24-84 months | $5000- $100,000 |

| J.J.Best Banc &Co | Rate Unavailable | 60-84 months | $6000-$2,000,000 |

| DCU | 9.24%-11.74% | Up to 84 months | A percentage of the car's appraised value (up to 90%) |

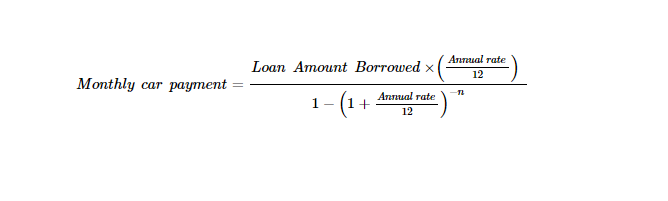

To calculate how much car loan you can afford, you should look for your budget to determine the amount of monthly payment you can afford.

The formula for calculating the monthly payment is shown below:

Where n represents the total number of payments made over the loan term

For example, if you can afford a monthly payment of $300, and the loan is for 5 years with an annual percentage rate of 5%, then the loan amount that you can borrow or that is affordable for you can be calculated as below:

Annual rate, 5% = 0.05

Total number of payments made over the loan term, n = 12×5 = 60

On solving, the loan amount that he can afford to borrow is found to be $15897.212.

Are you prepared to apply for a loan to fund the purchase of a classic car? Following these guidelines can shorten the procedure and help you secure the most advantageous loan terms possible.

Think about your chances of getting a loan based on your credit scores. You'll need good to exceptional credit with some lenders to qualify for a loan to purchase a classic car. Yet there is at least one notable deviation from this norm. But certain lenders are ready to work with borrowers with credit ratings as low as 600.

Those looking to finance a historic automobile typically work with expert classic car lenders that know how to put a fair value on a vehicle that is potentially older than the buyer. You may also compare rates offered by conventional auto loan providers by shopping around.

The lower the amount you finance, the cheaper your monthly payment; hence, the cost of the car you'll pay will be lower. The down payment on a classic car loan might be as high as 20%, though some lenders may waive this requirement. For example, classic car loans from J.J. Best Banc & Co. typically require a 20% down payment.

Dependent on your state's regulations, you may be legally required to have auto insurance. You may require classic automobile insurance for your prized vehicle. The market value of an automobile is used to determine the premiums for standard insurance policies; however, this may not reflect the true value of an older vehicle or the cost to repair it.

The value of a collector car is set at the outset of the policy. Although insurance for daily use is available, prices can be reduced by reducing the number of miles driven annually. As a bonus, some insurance policies include emergency roadside assistance coverage, which is especially useful for those driving older vehicles.

Classic car loans share many similarities with traditional auto loans, including the terms and procedures involved. There are, however, a few key distinctions.

Some of the major requirements of a classic car loan are:

The loan amount and the interest rate associated with a classic car loan will be determined by your financial condition, just as regular auto loans. Lenders use credit scores to determine whether a loan applicant is reliable concerning making loan repayments on time.

Generally, the higher a person's credit score, the more favorable conditions and interest rates they will be offered. If your credit score is low, lenders will assume you have a higher propensity to default on your loan payments. Consequently, your loan's interest rate will be higher to compensate for the lender's increased concern. Financing a classic car when you have a low credit score is difficult.

The minimum credit score to qualify for a loan will differ among lenders. For example, some classic automobile lenders may need a credit score of 700 or higher before extending credit for a loan.

Depending on your financial condition, there may be better alternatives to traditional auto loans for financing your classic or older used vehicle. Some of these are mentioned below:

A classic car could be within your budget if you take out a personal loan. A personal loan's interest rate is negotiated with the borrower based on their income and credit history and is often cheaper than those you'd get with a credit card. Your classic car could be used as collateral in case of a secured personal loan, but the lack of collateral for an unsecured loan could result in higher interest rates.

Another option for financing a classic car is a home equity loan. You can get a loan based on the value of your property or "equity." You will be required to repay a predetermined sum of money during the agreed-upon time frame.

Depending on the value of your property, a home equity loan could permit you to buy a more expensive vehicle than a standard auto loan or a personal loan. However, your home could be repossessed if this loan is not repaid. Compare the rates of interest and monthly payments of both car loans and home equity loans with the help of a loan calculator.

Leasing a classic car is an alternative to purchasing one. Classic vehicle lease payments are calculated similarly to regular auto lease payments: by looking at the automobile's estimated resale price. At the end of the lease period, you could buy the vehicle entirely, return it in exchange for the remaining lease payment, or enter into a new lease.

You may put that money toward a more expensive classic car if you don't need to make a sizable down payment (as you might with a loan). Shorter leases are available; you can even switch classic automobiles out mid-lease if you choose.

No matter what you decide to do-buy, lease, or borrow-you will be taking on a significant financial commitment. While it's understandable to have a strong connection to a classic car, letting your emotions cloud your judgment could cost you thousands. When purchasing a car, it's important to inspect it by either yourself or a professional to be sure you're receiving what you expect. And no matter how deeply you've fallen in love with a classic car, you should never finance one you can't afford. If you get behind on your payments, all that affection will vanish instantly.

In short, yes! Most lenders don’t usually cover for car loans. They are likely to finance a classy car with an interest rate slightly higher than that for new cars.

The duration varies based on the lenders. Some lenders may loan you a classic car loan for as long as 15 years.

As with most financing forms, the best interest rates are reserved for people with excellent credit histories and high FICO scores (often 661 and above).

In most cases, even with a high credit score, a bank will not approve financing for a vehicle over ten years old.